Welcome to this week's “Free-Rider Friday.” Most of our shows are “topic” driven, where we dive deep into one subject. Free-Rider Fridays are designed to be “event” driven—whatever issues are in the news that we (or you) find worthy of commentary. In economics, free riding means reaping the benefits from the actions of others and consequently refusing to bear the full costs of those actions. This means Ed and Ron will free ride off of the news, and each other, with no advanced knowledge of the events either will bring up.

The Soul of Enterprise: Dialogues on Business in the Knowledge Economy is now available on Amazon Kindle

Cover

Ed and I are pleased to announce the publication of our first book together, based on the topics from our show.

The book is available exclusively on Amazon Kindle. You can download the Kindle app for free to read the book on a device other than a Kindle.

The book contains six chapters, which are from our show, combined into logical topics. We also added an Introduction and Epilogue.

Further, we’ve added links to many of the ideas, definitions, books, and other interesting things we cite. It’s a complete digital experience.

The Foreword was written by VeraSage Instiute’s G. Robert Newhart Non-Value-Added Fellow, Greg Kyte, and it does not disappoint. There’s also some funny illustrations by the cartoonist, caricaturist and illustrator Andrew Fyfe from Australia, a pure genius.

Here’s a more detailed description of the book:

The world’s economy has been transformed from a twentieth-century materials-based economy to the Age of the Knowledge-Based Economy — and the currency of this realm is ideas, imagination, creativity, and knowledge. According The World Bank, 80% of the developed world’s wealth now resides in human capital.

Perhaps President Ronald Reagan said it best in his address to Moscow State University on May 31, 1988:

Like a chrysalis, we’re emerging from the economy of the Industrial Revolution — an economy confined and limited by the Earth’s physical resources — into, as one economist titled his book, “the economy in mind,” in which there are no bounds on human imagination and the freedom to create is the most precious natural resource.

Written by Ronald Baker and Ed Kless, hosts of The Soul of Enterprise: Business in the Knowledge Economy, the popular radio show on Voice America’s Business Channel, The Soul of Enterprise: Dialogues on Business in the Knowledge Economy sounds the clarion call that organizations can no longer ignore this seismic shift that has occurred in the economy since 1959. The Soul of Enterprise introduces the three components of Intellectual Capital — human capital, social capital, and structural capital — and how to leverage them to create wealth in today’s economy, by revealing:

The physical fallacy — why wealth no longer consists of tangible things, but of ideas, imagination and knowledge from human minds

The best learning tool ever invented: After Action Reviews

Why Frederick Taylor and the Scientific Management movement was a fraud and the wrong focus for knowledge workers

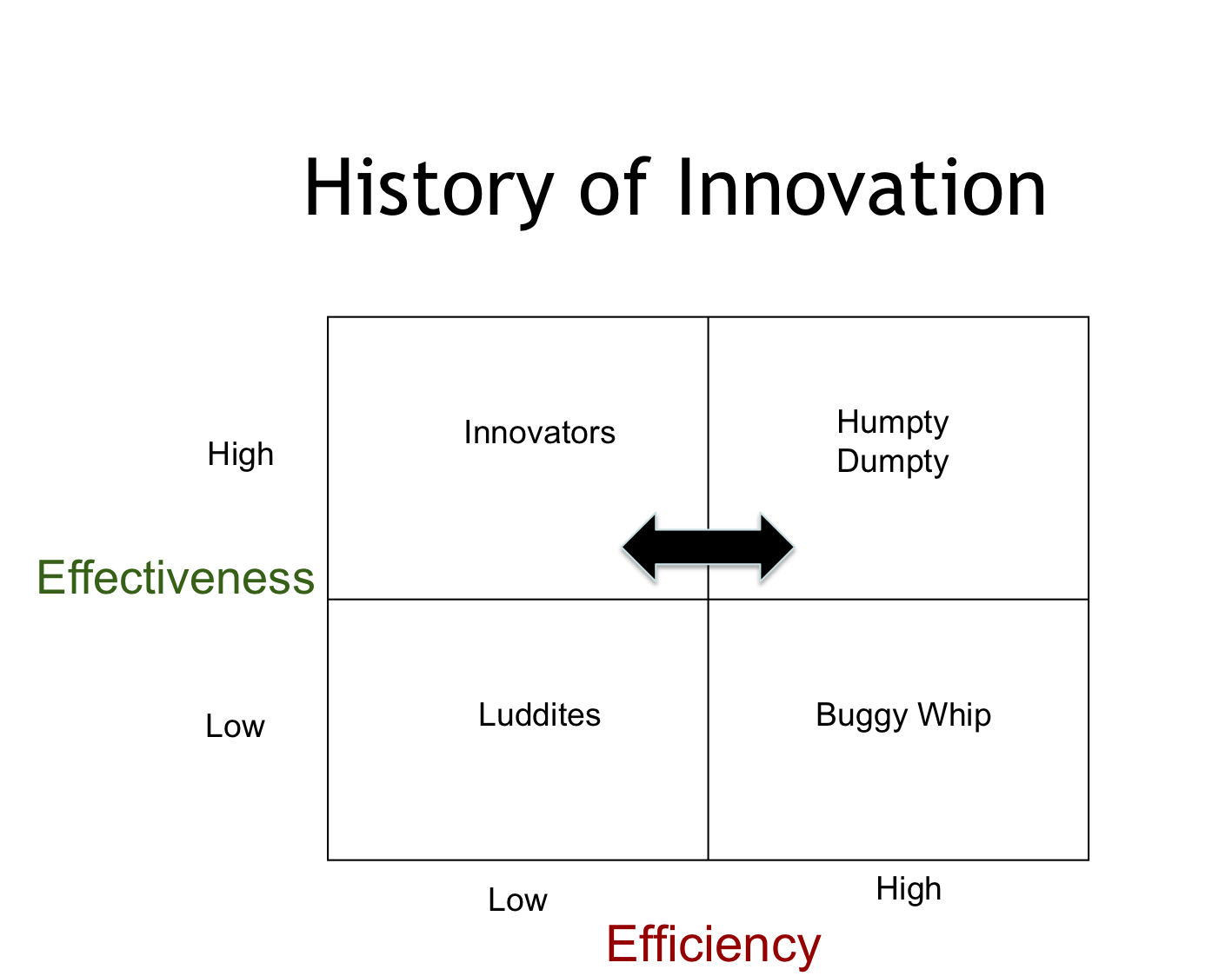

The fact that effectiveness always and everywhere trumps efficiency

The First Law of Pricing: All value is subjective

The Second Law of Pricing: All prices are contextual

The Morality of Markets: Doing well and doing good

Why your organization — and you — need to be driven by a higher purpose than profit

The Soul of Enterprise will inspire and challenge readers to unlock the enormous financial and competitive power hidden in the intellectual capital of their organizations and knowledge workers.

Bill Gates Doesn’t Understand Wealth Creation

Ron mentioned an article from The Economist’s The World in 2015, written by Bill Gates. Some excerpts:

…disease and extreme poverty are not inevitable. In the past 25 years, the number of children who die has dropped by a half. …The number of extremely poor people has been going down at roughly the same rate.

We also know why people are escaping poverty: it is thanks to more productive agriculture, better access to financial services, and the spread of functioning health systems that prevent expensive medical emergencies.

Is he kidding? What’s caused people to escape bone-crushing poverty is the spread of capitalism. Free markets are the cause of all the results he cites, yet he doesn’t seem to understand how markets work.

This never ceases to amaze me. Some of the most successful entrepreneurs, and wealthiest, have no idea how capitalism works. They were able to practice it, but they can’t explain it, or offer a theory in its defense.

It validates William F. Buckley Jr.’s quip: “ The problem with capitalism is capitalists.”

Net Neutrality

Next we discussed the thorny issue of net neutrality. We are both against the recent regulations from the FCC that reclassifies the Internet from an “information service” to a “telecommunication service.”

Can you point to one innovative, heavily regulated industry? Had the government regulated the early days of the computer revolution, we’d probably have Vacuum Tube Valley, most likely in West Virginia.

Even The Economist likes broad rules (fast lanes can’t exceed slow lanes by a certain amount), rather than blanket regulations.

There’s an excellent article by Nick Gillespie at Reason magazine on this issue.

In all fairness, no one has seen the regulations yet. But is there any doubt that once regulation starts, it expands?

Could it be used to require all websites to have a license? Or control content?

I’m sure we will discuss this topic in future shows.

Greg Kyte

Greg Kyte called for the latter half of the show, discussing his work, videos, the Foreword he wrote to our book, and his new business: ComedyCPE.com.

Watch some of his hilarious videos at GregKyte.com, including the above infamous series of queuing up for the Blackberry, Bob’s BBQ, Great Moments in Value Pricing History, Parts I and II, and Billable Hour Scratch & Win.